The Hidden Danger of Unmapped Flood Zones

How Gaps in Flood Data Put Homes and Communities in Danger.

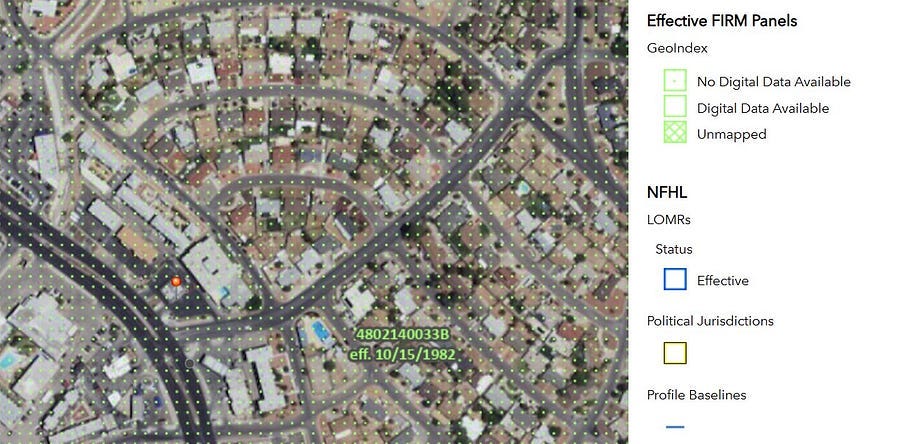

When a property sits outside a FEMA high-risk flood zone, it often feels like a green light. But the absence of a flood zone designation on the map doesn’t mean the absence of risk. Across the U.S. — and especially in fast-growing states like Florida, Texas, and Nevada — thousands of communities remain unmapped, under-mapped, or reliant on outdated flood studies. The consequences are very real. In August 2025, a flash flood swept across El Paso’s Mesa Street, overwhelming drainage and stranding vehicles in minutes. The area — mapped but not updated since 1982 (FIRM Panel 4802140033B) — was a stark reminder that a gap on the map doesn’t mean it’s safe (reported by KFOX14).

The real question is: what should buyers, owners, and local governments keep in mind when flood maps don’t tell the full story?

The Key Things to Know

The Limits of FEMA Maps

FEMA’s Flood Insurance Rate Maps (FIRMs) don’t cover every square mile. Large rural areas, inland basins, and even some urban developments may sit in Zone D (undetermined risk) or carry the vague label “Not Printed.” That doesn’t mean “safe” — it means “unknown.” In fact, a recent NBC News report shows that roughly 75% of FEMA’s flood maps are outdated. For homeowners, areas with no detailed mapping — whether Zone D, Not Printed, or simply outdated — can hide the same risks as a Special Flood Hazard Area. To explore current flood maps, flood studies, or Letters of Map Change (LOMCs) for your specific location, visit FEMA’s Flood Map Service Center, the official resource for detailed flood hazard information

Key takeaway: Ask your local floodplain administrator whether a Base Flood Elevation (BFE) exists, if new studies are in progress, or if the area has a history of flooding not captured on the map.

Understanding FEMA Map Gaps: Unmapped and Not Printed Areas

FEMA’s flood maps are widely used tools, but their terminology can create confusion. Two categories often misunderstood are unmapped and not printed.

Unmapped areas are places where FEMA has not performed a flood study or published any hazard data. These are often assigned Zone D, meaning the risk is undetermined.

Not printed panels exist in FEMA’s system but were not published as detailed maps because the entire area fell into a single, usually low-risk flood zone. On index maps, they appear with the label “Not Printed.”

Despite the difference, both share the same critical weakness: they leave flood risk largely unrepresented. Neither should be mistaken for “safe.”

Hidden Localized Hazards

Even where maps exist, they don’t capture everything. Drainage ditches that overflow in summer storms, sheet flow across flat terrain, or runoff from a new subdivision uphill can all trigger flooding beyond the official lines. My friend learned this the hard way when her rural Florida cabin — located in a “Not Printed” panel, not an unmapped area — flooded after just one heavy storm.

After one heavy storm, the same property was surrounded by floodwater.

Key takeaway: Look beyond FEMA maps. Visit the site after rainfall, talk with neighbors, local floodplain administrator, or insurance claims history.

The Future That Maps Don’t Show

Flood maps are only a snapshot in time. They capture past studies but don’t account for new development, increases in impervious surface, or the broader impacts of climate change. Communities that rely solely on FEMA maps risk under-preparing for the floods of tomorrow.

Key takeaway: Watch for updated studies from FEMA or state agencies, and support local initiatives that go beyond minimum standards — like requiring freeboard (building a foot or two higher than the mapped flood level) or encouraging FEMA to incorporate future conditions such as climate change, new development, and updated rainfall patterns into their maps.

The Implications

FEMA’s flood maps remind us of a hard truth: they’re only the starting point, not the full picture. From rural cabins to urban neighborhoods, gaps in FEMA’s maps — whether unmapped, not printed, or simply outdated — are a silent threat that can upend lives and finances in a single storm. Historically, it took disasters — like the 1960s floods that spurred the creation of the National Flood Insurance Program — for policy to catch up with reality.

The open question is whether we will wait for the next flood to reveal the gaps — or proactively close them by demanding better data, stronger standards, and smarter local planning.

Disclaimer: The views expressed here are solely my own and do not reflect those of any public agency, employer, or affiliated organization. It empowers readers with objective geographic and planning insights to encourage informed discussion on global and regional issues.